0 简介

今天学长向大家介绍一个机器视觉的毕设项目

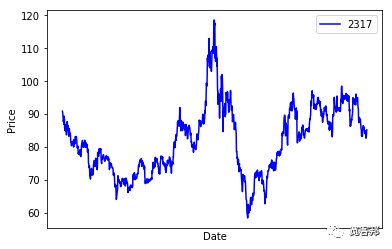

毕业设计项目分享 LSTM股价预测

项目运行效果:

毕业设计 lstm股价预测

项目获取:

https://gitee.com/sinonfin/algorithm-sharing

1 LSTM 神经网络

长短期记忆 (LSTM) 神经网络属于循环神经网络 (RNN) 的一种,特别适合处理和预测与时间序列相关的重要事件。以下面的句子作为一个上下文推测的例子:

“我从小在法国长大,我会说一口流利的??”

由于同一句话前面提到”法国“这个国家,且后面提到“说”这个动作。因此,LSTM便能从”法国“以及”说“这两个长短期记忆中重要的讯号推测出可能性较大的”法语“这个结果。

K线图与此类似,股价是随着时间的流动及重要讯号的出现而做出反应的:

- 在价稳量缩的盘整区间中突然出现一带量突破的大红K,表示股价可能要上涨了

- 在跳空缺口后出现岛状反转,表示股价可能要下跌了

- 在连涨几天的走势突然出现带有长上下影线的十字线,表示股价有反转的可能

LSTM 要做的事情就是找出一段时间区间的K棒当中有没有重要讯号(如带量红K)并学习预测之后股价的走势。

2 LSTM 股价预测实例

数据是以鸿海(2317)从2013年初到2017年底每天的开盘价、收盘价、最高价、最低价、以及成交量等数据。

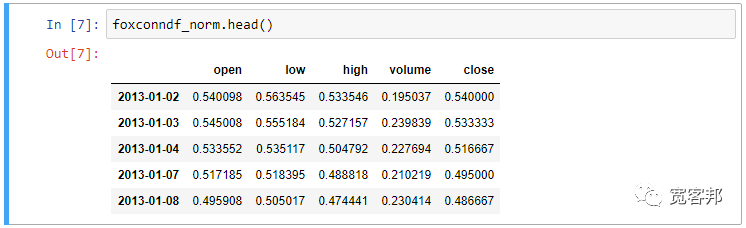

首先将数据写入并存至pandas的DataFrame,另外对可能有N/A的row进行剔除:

数据写入:

import pandas as pd

foxconndf= pd.read_csv('./foxconn_2013-2017.csv', index_col=0)

foxconndf.dropna(how='any',inplace=True)

為了避免原始数据太大或是太小没有统一的范围而导致 LSTM 在训练时难以收敛,我们以一个最小最大零一正规化方法对数据进行修正:

from sklearn import preprocessing

defnormalize(df):

newdf= df.copy()

min_max_scaler = preprocessing.MinMaxScaler()

newdf['open']= min_max_scaler.fit_transform(df.open.values.reshape(-1,1))

newdf['low']= min_max_scaler.fit_transform(df.low.values.reshape(-1,1))

newdf['high']= min_max_scaler.fit_transform(df.high.values.reshape(-1,1))

newdf['volume']= min_max_scaler.fit_transform(df.volume.values.reshape(-1,1))

newdf['close']= min_max_scaler.fit_transform(df.close.values.reshape(-1,1))return newdf

foxconndf_norm= normalize(foxconndf)

然后对数据进行训练集与测试集的切割,另外也定义每一笔数据要有多长的时间框架:

import numpy as np

def data_helper(df, time_frame):

3 数据维度: 开盘价、收盘价、最高价、最低价、成交量, 5维

number_features = len(df.columns)

# 将dataframe 转换为 numpy array

datavalue = df.as_matrix()

result = []

# 若想要观察的 time_frame 為20天, 需要多加一天作为验证答案

for index in range( len(datavalue) - (time_frame+1) ): # 从 datavalue 的第0个跑到倒数第 time_frame+1 个

result.append(datavalue[index: index + (time_frame+1) ]) # 逐笔取出 time_frame+1 个K棒数值做為一笔 instance

result = np.array(result)

number_train = round(0.9 * result.shape[0]) # 取 result 的前90% instance 作为训练数据

x_train = result[:int(number_train), :-1] # 训练数据中, 只取每一个 time_frame 中除了最后一笔的所有数据作为feature

y_train = result[:int(number_train), -1][:,-1] # 训练数据中, 取每一个 time_frame 中最后一笔数据的最后一个数值(收盘价)作为答案

# 测试数据

x_test = result[int(number_train):, :-1]

y_test = result[int(number_train):, -1][:,-1]

# 将数据组成变好看一点

x_train = np.reshape(x_train, (x_train.shape[0], x_train.shape[1], number_features))

x_test = np.reshape(x_test, (x_test.shape[0], x_test.shape[1], number_features))

return [x_train, y_train, x_test, y_test]

4 以20天为一区间进行股价预测

X_train, y_train, X_test, y_test = data_helper(foxconndf_norm,20)

我们以 Keras 框架作为 LSTM 的模型选择,首先在前面加了两层 256个神经元的 LSTM

layer,并都加上了Dropout层来防止数据过度拟合(overfitting)。最后再加上两层有不同数目神经元的全连结层来得到只有1维数值的输出结果,也就是预测股价:

from keras.models import Sequential

from keras.layers.core import Dense, Dropout, Activation

from keras.layers.recurrent import LSTM

import keras

defbuild_model(input_length, input_dim):

d =0.3

model = Sequential()

model.add(LSTM(256, input_shape=(input_length, input_dim), return_sequences=True))

model.add(Dropout(d))

model.add(LSTM(256, input_shape=(input_length, input_dim), return_sequences=False))

model.add(Dropout(d))

model.add(Dense(16,kernel_initializer="uniform",activation='relu'))

model.add(Dense(1,kernel_initializer="uniform",activation='linear'))

model.compile(loss='mse',optimizer='adam', metrics=['accuracy'])return model

# 20天、5维

model = build_model(20,5)

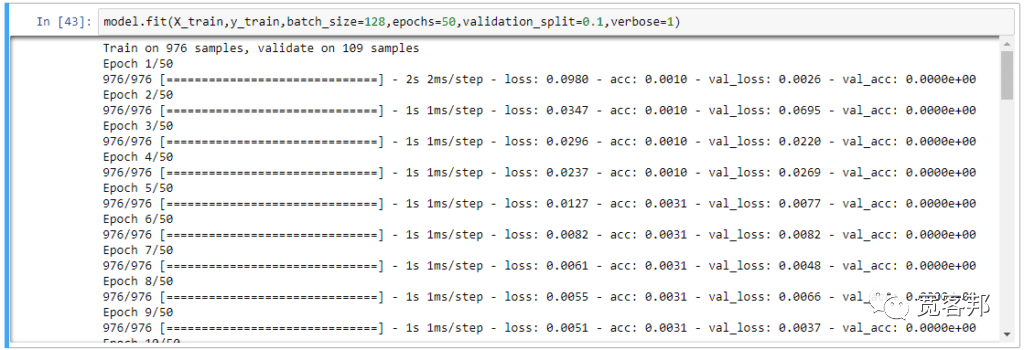

建立好 LSTM 模型后,我们就用前面编辑好的训练数据集开始进行模型的训练:LSTM 模型训练

# 一个batch有128个instance,总共跑50个迭代

model.fit( X_train, y_train, batch_size=128, epochs=50, validation_split=0.1, verbose=1)

在经过一段时间的训练过程后,我们便能得到 LSTM

模型(model)。接着再用这个模型对测试数据进行预测,以及将预测出来的数值(pred)与实际股价(y_test)还原回原始股价的大小区间:

LSTM 模型预测股价及还原数值

defdenormalize(df, norm_value):

original_value = df['close'].values.reshape(-1,1)

norm_value = norm_value.reshape(-1,1)

min_max_scaler = preprocessing.MinMaxScaler()

min_max_scaler.fit_transform(original_value)

denorm_value = min_max_scaler.inverse_transform(norm_value)return denorm_value

# 用训练好的 LSTM 模型对测试数据集进行预测

pred = model.predict(X_test)# 将预测值与实际股价还原回原来的区间值

denorm_pred = denormalize(foxconndf, pred)

denorm_ytest = denormalize(foxconndf, y_test)

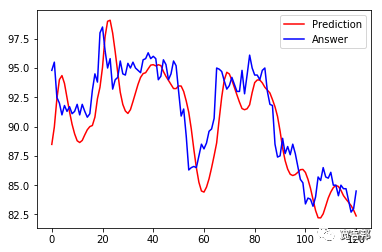

5 LSTM 预测股价结果

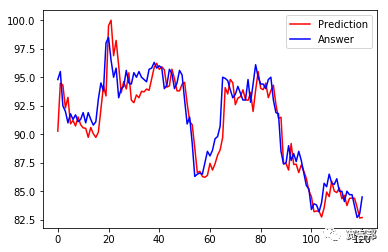

让我们把还原后的数值与实际股价画出来,看看效果如何:

LSTM 预测股价结果

import matplotlib.pyplot as plt

%matplotlib inline

plt.plot(denorm_pred,color='red', label='Prediction')

plt.plot(denorm_ytest,color='blue', label='Answer')

plt.legend(loc='best')

plt.show()

如下图,蓝线是实际股价、红线是预测股价。虽然整体看起来预测股价与实际股价有类似的走势,但仔细一看预测股价都比实际股价落后了几天。

所以我们来调整一些设定:

- 时间框架长度的调整

- Keras 模型里全连结层的 activation 与 optimizaer 的调整

- Keras 模型用不同的神经网路(种类、顺序、数量)来组合

batch_size的调整、epochs的调整 …

经过我们对上述的几个参数稍微调整过后,我们就得到一个更贴近实际股价的预测结果啦。

6 完整工程项目

项目分享:

版权归原作者 A毕设分享家 所有, 如有侵权,请联系我们删除。